- Forward Guidance

- Posts

- 🟠 Up in the air*

🟠 Up in the air*

Plus, BTC’s latest run and rising initial jobless claims

Ben Strack & Felix Jauvin

December 05, 2024

Welcome to the Forward Guidance newsletter, brought to you by Casey Wagner, Ben Strack and Felix Jauvin. Here’s what you’ll find in today’s edition:

Felix breaks down why the Fed’s expected next move could be a mistake.

Jobs data week continues with an increase in initial claims.

BTC’s new ATH could spur further momentum. But don’t forget about volatility.

Fed lost at sea?

There’s a lot of confusion about why the Fed might still be cutting rates right now despite what looks to be an economy that is doing pretty well.

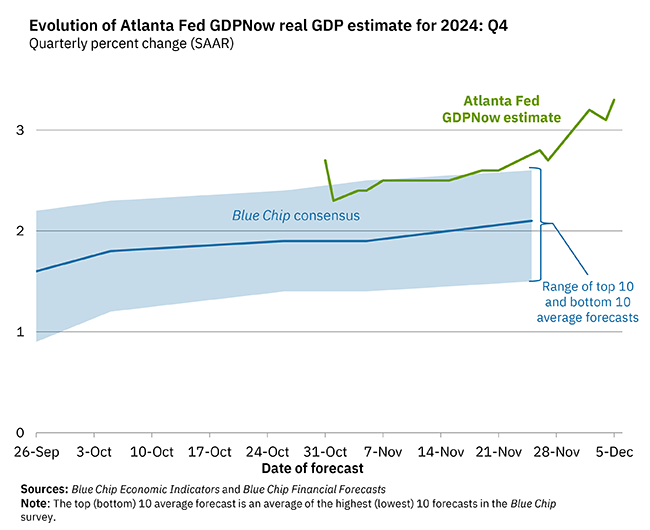

The Atlanta Fed GDPNow is currently forecasting a 3.3% real GDP growth rate for Q4, and it looks to be accelerating:

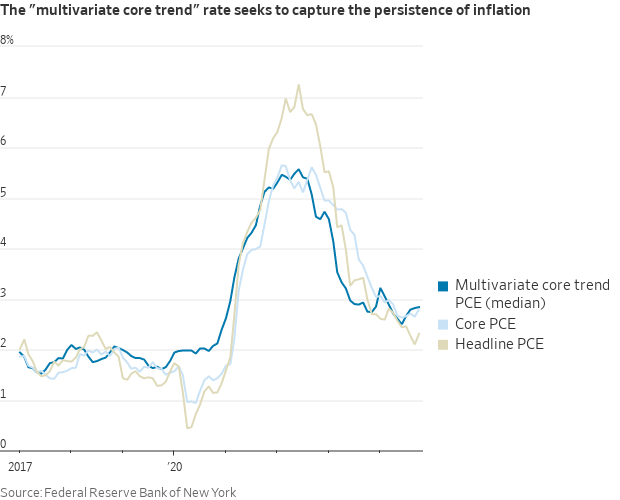

Further, it looks like inflation is beginning to rebound and has bottomed:

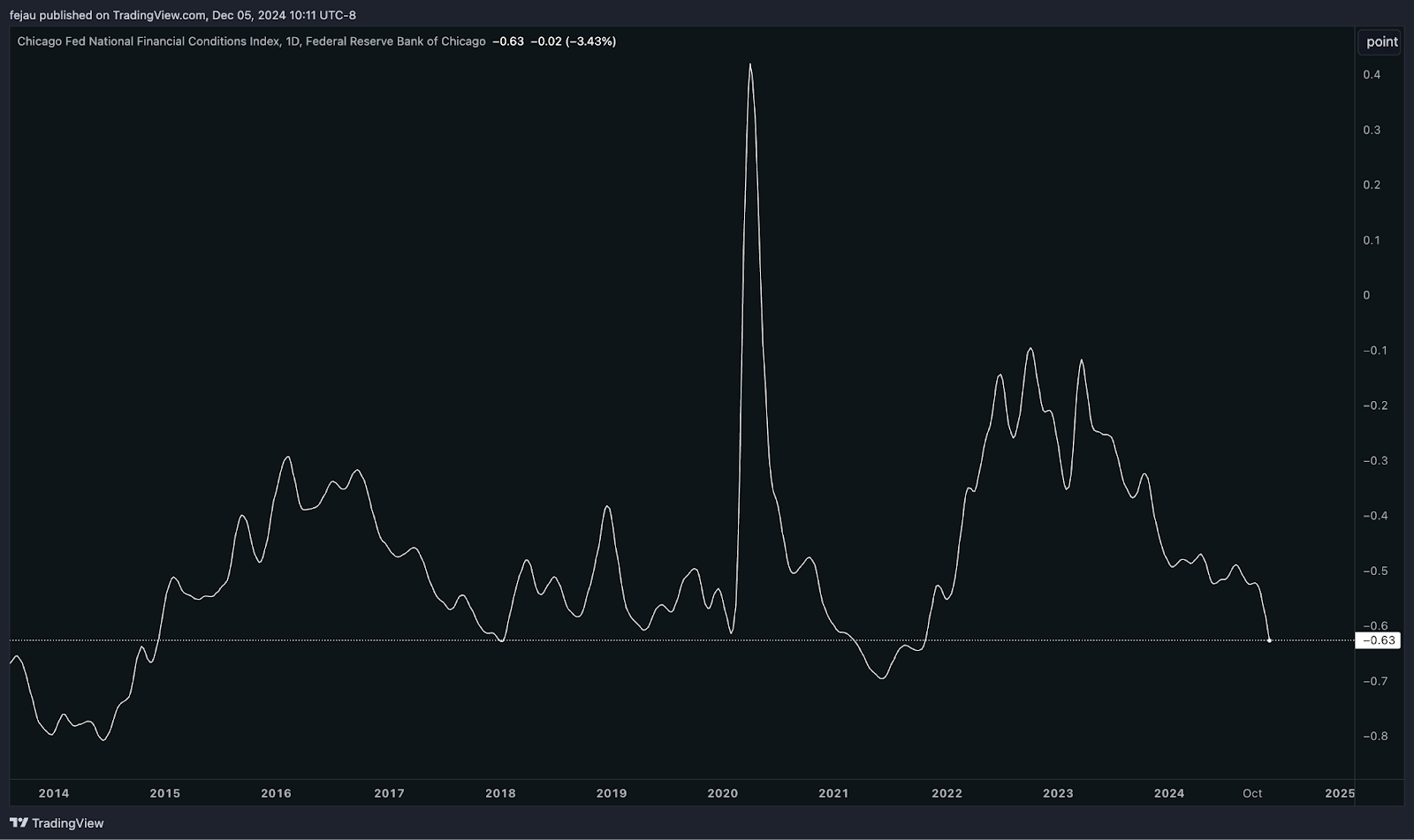

Also, financial conditions are nearly as loose as they were during the frothy 2021 era:

Despite all these metrics characterizing an economy that is doing very well, the FOMC is still sitting at a 70% odds of cutting rates this December. This has many people perplexed as to why they would still cut.

The simple reason is that the committee had already guided the market toward them cutting in December. They would hate to rock the boat, reverse that guidance and skip when the forward curve has already assumed they likely will.

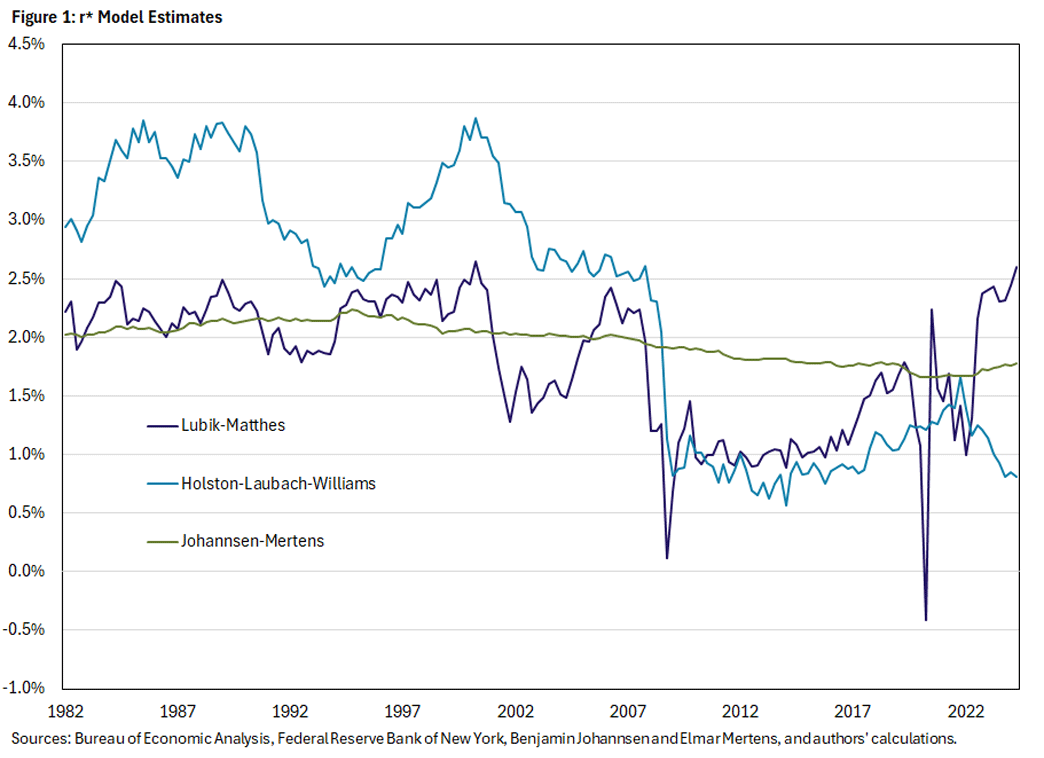

The more interesting answer resides in the rationale behind why they guided toward this cut in the first place. It has to do with r* — the neutral interest rate — and how the Fed measures it.

Because r* cannot be directly measured within the economy, policymakers instead rely on models that do their best attempt at estimating it. There are currently two models well-suited for this job: the Lubik model and the Williams model.

The Lubik model is more dynamic and based on a statistical model approach, whereas the Williams model is based on more traditional macroeconomic models that are less sensitive to major shifts in the drivers of r*.

Considering that the creator of the Williams model — John Williams — is the current NY Fed president, this model is weighted more heavily within the confines of the Fed compared to the Lubik model.

As we can see in the chart below, the Lubik model has picked up a significant uptick in r*, whereas the Wiliams model remains at a secular low.

Because of this adherence to the Williams model, the FOMC continues to strongly believe monetary policy is very restrictive, and that they could easily cut to 4% and remain restrictive.

However, if we use the Lubik model instead, there’s an argument to be made that monetary policy is already at neutral (at a bare minimum).

Empirically (as observed in the charts at the beginning of this piece), market signals are firing off all over the place that we are in a very accommodative environment from a policy perspective. Therefore, it’s reasonable to assume the Williams model is incorrect when compared to what we’re experiencing in markets and the economy right now.

There’s been a lot of talk from FOMC members lately around where they believe neutral might be. This suggests members might be rethinking their adherence to the Williams model. Some FOMC members, such as Austan Goolsbee, are even preferring to “feel their way” to neutral. See how the economy reacts, and go from there.

Considering how markets across the board continue to hit all-time highs on a daily basis, it’s hard to make the argument that we’re restrictive. Regardless, a cut in December still looks to be the base case as the FOMC remains anchored to bureaucratic inertia with respect to the Williams model.

— Felix Jauvin

This is the number of jobs analysts expect the US economy added last month. Remember, nonfarm payrolls added 12,000 positions in October, a dip largely attributed to Boeing layoffs and back-to-back hurricanes in the Southeast.

If we can get into the 200,000 range tomorrow, it’s likely FOMC members will opt for one more 25bps cut to close out the year. If the number comes in wildly larger (and I mean wildly, as it would take a lot), those hopes start to dwindle.

It seems fitting that bitcoin’s rise above $103,000 came in the final month of a groundbreaking year for the asset.

You already know about the first US spot bitcoin ETFs in January and Trump’s election win a month ago. Then there was the president-elect’s selection this week of Paul Atkins as SEC chair (who many deem to be a crypto advocate). And Fed Chair Jerome Powell even recently compared bitcoin to gold.

The fact that gold’s market cap is still nine times larger than bitcoin’s (about $18T to $2T) “should offer additional insight into how much more room there is for bitcoin to grow from current levels," LMAX Group market strategist Joel Kruger said in an email.

Momentum driving BTC past the psychological six-figure price mark can beget more momentum — albeit not without volatility.

“It not only validates the long-term belief of the community but also signals to institutions, corporations, sovereign funds, skeptics and sidelined investors alike that bitcoin has entered a new phase of adoption and recognition as a store of value and a transformative asset class,” according to 21Shares crypto research strategist Matt Mena.

A key next target is $110,000, Mena added, citing Deribit data that shows the majority of Jan. 31, 2025 call option contract volume is concentrated at that price level.

Industry watchers have also pointed to BTC’s history of price swings to temper mania from the most bullish of bulls.

After the early years of bitcoin, the road to $100,000 included a rise to $18,000 in 2017 followed by a plummet to around $4,000 the following year. A surge to nearly $70,000 in late-2021 was followed by a severe downward move to $16,000 in 2022.

While optimism is high that the Trump Administration and a crypto-friendly Congress will help spur crypto regulatory and legislative clarity, Nansen principal research analyst Aurelie Barthere said those might not pan out as expected.

He said: “Once we witness the first policies and decisions from the Trump Administration in January, there could be some risk of disappointed expectations, especially if the agenda prioritizes tariff and immigration-related policies first.”

— Ben Strack

Jobs week continues with the latest initial claims report released this morning. The data came in a bit mixed, but is overall consistent with the 13-week moving average. These numbers are also the first we are getting in the holiday season, which is known as a volatile period.

Initial jobless claims rose in the week ended Nov. 30, coming in at 224,000. This was a bit higher than analysts’ expectations of 215,000+ from the week prior, which was upwardly revised to 217,500.

States with the biggest increases in initial claims include Pennsylvania and Kentucky.

The overall 13-week moving average for initial claims is 226,000.

Continuing claims eased a bit from 1.9 million a week prior to 1.87 million last week. Analysts had expected no change.

Expectations for a 25-basis point interest rate cut later this month eased on the report. Fed funds futures markets now price in a 29.9% chance of Fed officials leaving interest rates unchanged, up from 21.9% on Wednesday.

Stocks dipped a bit following the release, before paring gains later in the session. The S&P 500 and Nasdaq Composite indexes were trading relatively flat midway through Thursday’s session, down 0.04% and 0.06%, respectively, at 2 pm ET.

Bitcoin meanwhile hovered in the $101,000 range this afternoon, sustaining its rally sparked Tuesday evening when the largest cryptocurrency broke $100,000 for the first time ever. More on that, and what we can expect next, below.

We’ll need to see more Goldilocks data tomorrow in the November jobs report, which will be released at 8:30 am ET.

— Casey Wagner

We mentioned BTC’s price rise to six figures. Bitcoin was hovering around $100,400 at 2 pm ET — up 1.7% from 24 hours prior, but down from a few hours earlier. ETH was at $3,865 around that time after peaking above $3,950 just hours before.

BlackRock’s iShares Bitcoin Trust (IBIT) has hit $50 billion in assets less than 11 months after launching. It took the previous fastest-growing ETF — the iShares Core MSCI Emerging Markets ETF (IEMG) — about five times longer to reach that asset level, Bloomberg Intelligence’s Eric Balchunas pointed out.

Sol Strategies, a publicly traded Canadian company focused on the Solana ecosystem, on Thursday submitted its application to list on the Nasdaq.