- Forward Guidance

- Posts

- ✂️ Kicking the cut can

✂️ Kicking the cut can

The market doesn't expect a Fed rate cut anytime soon

Ben Strack & Felix Jauvin

February 13, 2025

Here’s what you’ll find in today’s edition:

The Fed is off to the races with its pause cycle.

Trump’s crypto advisory council may not be what the industry had hoped.

The perhaps surprising takeaways from another adviser survey on crypto.

The cutting cycle is dead. Long live the cutting cycle

A lot has changed in the six months since the Fed decided to cut rates.

If we rewind back to September, things looked very different:

The unemployment rate was looking weak and had surged to 4.2%, triggering the Sahm rule and causing a cacophony of concerns that a recession was imminent.

At the same time, inflation looked like it was close enough to the Fed’s 2% target that it could forego concerns about stable prices and hone in on supporting the labor market by beginning to cut the fed funds rate.

With this balance in mind, the Fed went ahead and cut 100 basis points in that time up until today:

During these months, it became easy to be complacent that we were set into an easing cycle and it was time to ride that wave.

However, coming back to the present day, the environment could not be more different. For all intents and purposes, the cutting cycle is over.

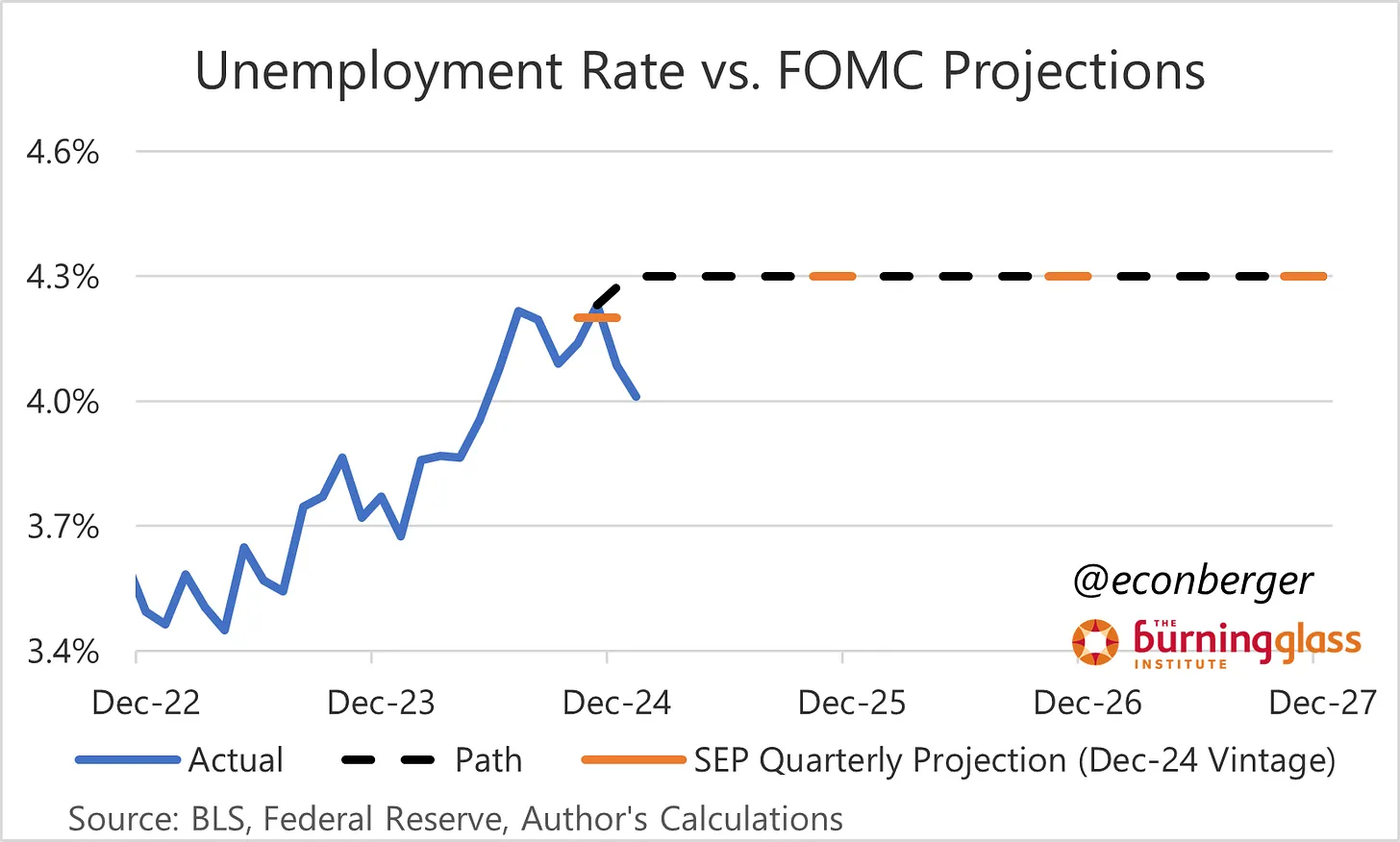

Looking at the labor market, it has improved significantly. Comparing the unemployment rate to the Fed’s forecast from only December, we can see that it has come down significantly.

Therefore, if one is looking to the employment side of the Fed’s dual mandate, there is no reason whatsoever for it to be easing at this juncture.

And so, the onus for any marginal easing from the Fed falls to the inflation side of the dual mandate.

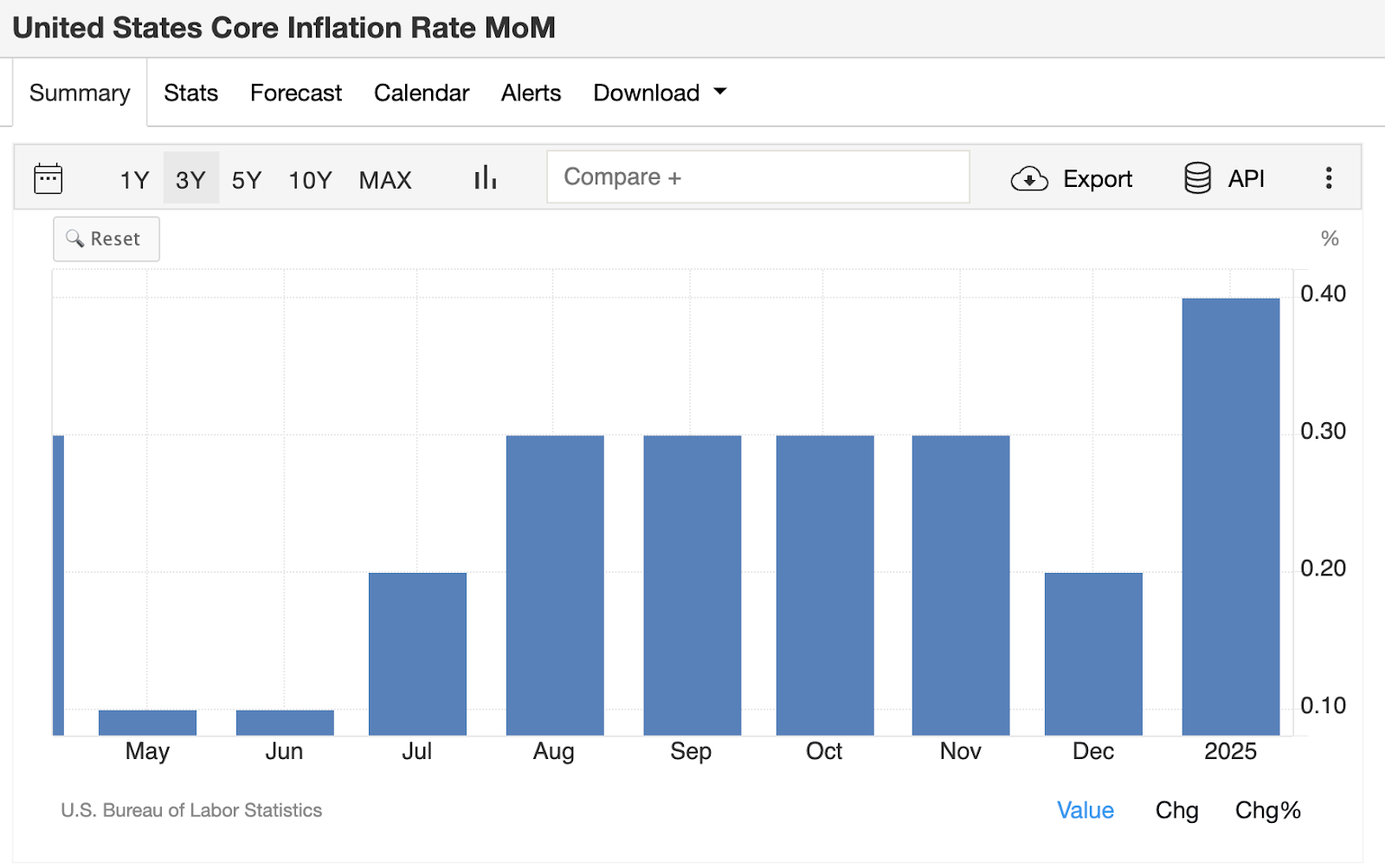

This week we received the CPI print for January, and it was a hot one by all accounts.

Core CPI came in at 0.4%, a notable jump higher from recent data.

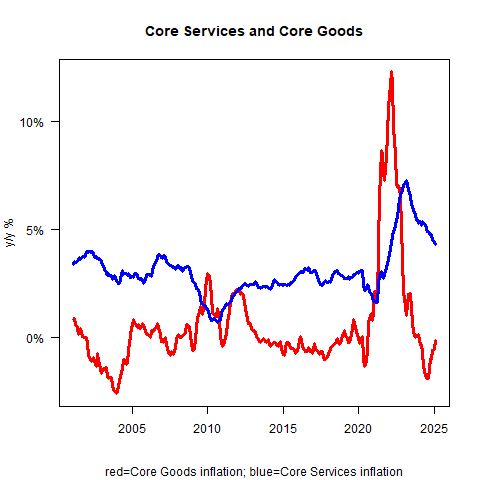

The theme of the inflation story over the last two years has been goods disinflating while services remain stubbornly high. As seen in the chart below, the major issue today is that goods are inflating again and services are refusing to take the baton of disinflation:

The simple takeaway from this granular data is that inflation is remaining above the Fed’s 2% target and bouncing around the 3-4% level. As long as this is occurring, there’s little reason for the Fed to cut rates when both sides of its dual mandate are seeing such strength.

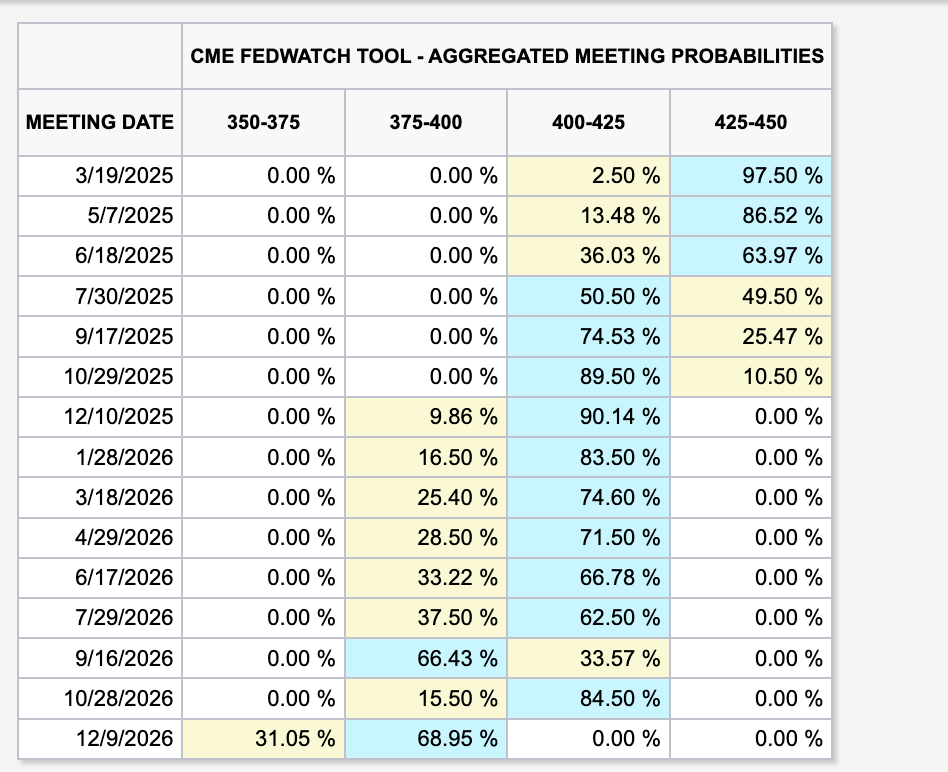

Putting it all together, we are now seeing a rate-cutting cycle that is seemingly over. As it stands today, the market has moved from expecting a rate cut in March to the end of this year instead:

If the data continues to come in above the Fed’s targets, it’s reasonable to think that these cuts will continue to get pushed out until they no longer exist.

— Felix Jauvin

Six weeks out from DAS NYC, and the stakes have never been higher.

How are fund managers positioning? What’s the real institutional play on ETFs, onchain finance, and global markets?

At DAS NYC, you’ll hear directly from the firms building their strategies around this:

Franklin Templeton on tokenization and the next phase of asset management.

Morgan Stanley Investment Management on how institutions are positioning in emerging markets.

Galaxy Digital on the investment landscape and how smart money is allocating.

If you’re coming, bring your team. Group passes are 25% off for 10+ people — but only until Feb. 14. Smaller groups (4-9) still save 15%.

📅 March 18-20 | NYC

The quarter-over-quarter increase in crypto transaction-based revenue for Robinhood — from $61 million in Q3 to $358 million in Q4.

That crypto-related revenue was more than half the company’s $672 million of transaction revenue seen in the last three months of 2024.

We’ll keep an eye on the Q4 results Coinbase is set to reveal later today and will report back.

President Trump’s crypto advisory council, established by executive order during his first week in office, may not be shaping up to be exactly what the industry had envisioned.

Unchained reported yesterday that the council may be scrapped altogether. In its place, according to unnamed sources, the Trump team would organize “policy summits” to discuss legislation with industry stakeholders.

I’ve also heard that policy summits are on the table. Two other sources familiar with the matter told me that if there’s an advisory council at all, it would likely be made up of government employees rather than industry executives.

It’s no secret that a lot of people wanted roles on that council. The NY Post reported there were at one point two dozen seats up for grabs, although I haven’t been able to confirm that figure.

What I’m hearing: Trump’s team is trying to avoid having too many cooks in the kitchen.

On the one hand, they’re in a tough spot. They want to avoid alienating certain sections of the industry — many of which were big donors during the campaign — but the act of bringing everyone together will lead to inter-industry conflict. Enter the “policy summit” pitch.

It wouldn’t be unprecedented. The House Financial Services GOP retreat earlier this month featured a 45-minute presentation and Q&A with a16z’s Chris Dixon, according to people familiar. Industry execs and lobbyists are on the Hill all the time trying to inform policy.

We’ll be monitoring the council situation. You just monitor your inbox.

— Casey Wagner

When it comes to crypto adoption, we’ve repeatedly heard how much room there is to run.

If you took a liquor shot every time someone said “early innings” at a crypto conference, you’d have trouble walking a straight line out of there. The need for “more education” is another phrase we hear ad nauseam.

But a recent CoinShares survey of financial advisers confirmed some of this, with specifics. We referenced one stat from it in yesterday’s edition (79% saying their role is shifting to risk management as clients invest in crypto on their own).

There are a few more worth pointing to. CoinShares CEO Jean-Marie Mognetti said he was perhaps most struck by a belief 62% of advisers hold: Recommending bitcoin doesn’t align with their obligation to act in their client’s best interest.

“This highlights a significant perception gap between regulatory approval, client demand and advisers' fiduciary concerns,” he told me.

Then there was the 55% who said recommending digital assets would harm their reputation with colleagues. This, Mognetti explained, “underscores the cultural and institutional barriers that still exist within traditional financial circles.”

It wasn’t long ago that Bitwise CIO Matt Hougan argued Trump’s election win and a pro-crypto Congress “removes the last vestige of reputational risk from crypto.”

Not everyone feels that way apparently, even with 85% of the advisers that CoinShares surveyed saying their organization’s sentiment toward crypto (and how they’re advising clients) changed since the election.

Another fascinating finding: Gen Z and Millennial advisers are more likely to think recommending speculative assets doesn’t align with their fiduciary duty — and to say that “threats outpace innovation.”

While this younger demographic is often more open to digital assets, they also seem to face “stronger resistance from more established industry norms and colleagues,” Mognetti said.

Back to the education point: Though 71% say their firm is educating them on crypto, 84% are likely to pay for such education (mostly via online courses and conferences).

Also, 43% of advisers cite crypto platforms publishing biased information as a barrier. So maybe read Forward Guidance instead.

— Ben Strack

President Trump on Thursday announced 25% tariffs on steel and aluminum imports from the EU and Asia as part of his promised reciprocal fees.

January’s PPI, which gauges wholesale prices, rose by 0.4% on the month, slightly above estimates.

Tune into the latest episode of the Forward Guidance podcast with Andreas Steno Larsen here or wherever you get your podcasts.