- Forward Guidance

- Posts

- 🚢 Bessent stays the course

🚢 Bessent stays the course

Unpacking the Treasury refunding statement

Ben Strack & Felix Jauvin

February 06, 2025

Here’s what you’ll find in today’s edition:

Felix dives into the latest quarterly refunding announcement.

After a rebrand, the largest “bitcoin treasury company” shares its 2025 targets.

A look at BTC’s evolving correlations to more traditional asset classes.

Big takeaways from Bessent’s first quarterly refunding announcement

With the recent confirmation of Scott Bessent as US Treasury Secretary, we’ve received the first quarterly refunding announcement under his leadership.

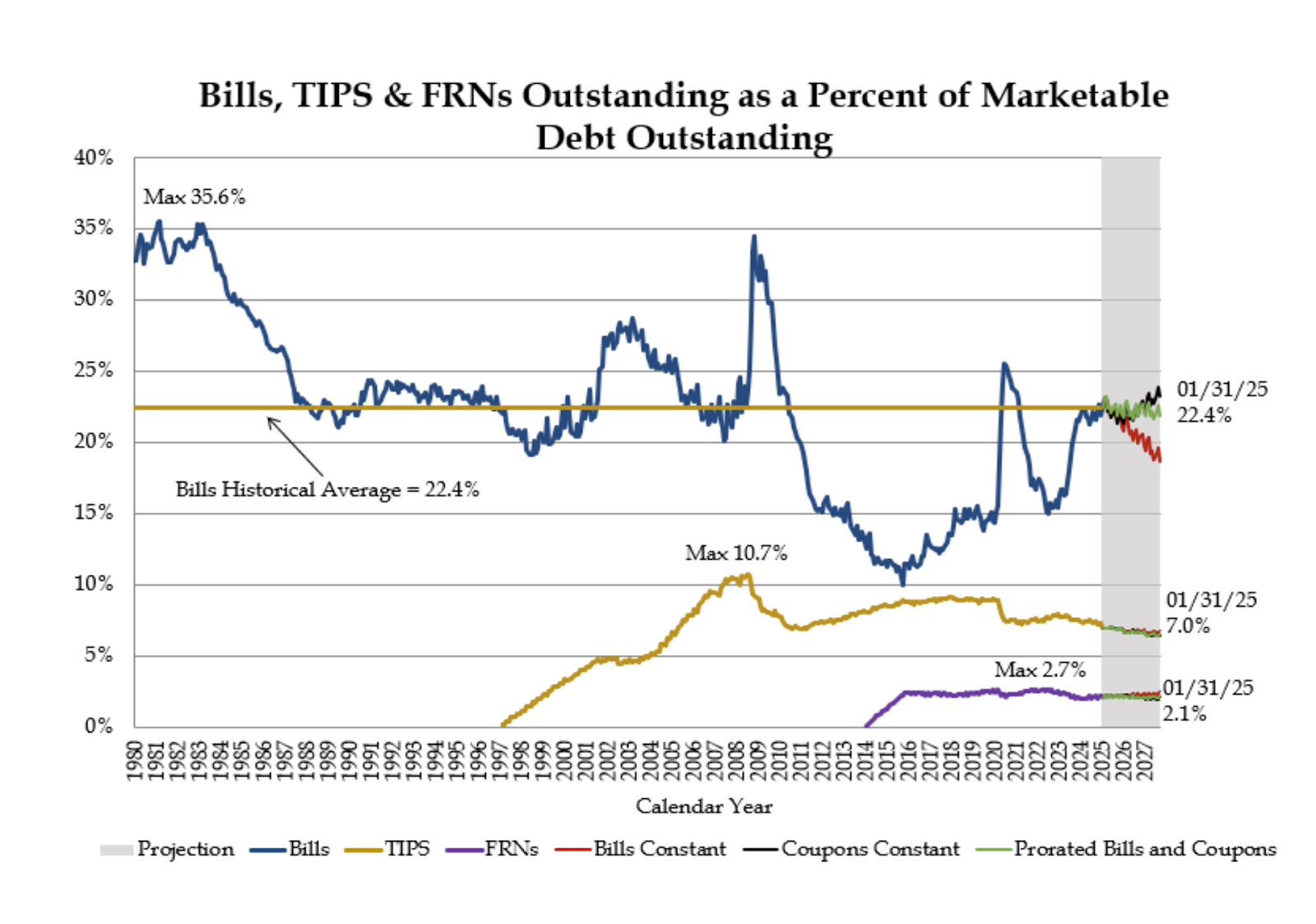

Much has been written in the past year about the potential politicization of the composition of debt being issued by Treasury and how that could impact markets.

As seen below, the proportion of bills that have been issued compared to coupons has skyrocketed. Historically, this type of maneuver has been kept for times of crisis when Treasury needs to raise a lot of money very quickly, with little impact to duration.

However, this has occurred in a regime of exceptional economic strength.

Before being nominated as secretary, Bessent was publicly critical of this strategy. He discussed his belief that it was essential for the composition of issued debt to get normalized — meaning an increase in proportion of longer-duration debt being issued.

Though admirable, this strategy would be very precarious due to the lack of structural demand for long-duration bonds without the Fed buying for QE, foreign central banks becoming net sellers of long-term debt, and concerns about fiscal deficits increasing.

With that context, all eyes were on this week’s QRA to see whether Bessent would change the composition of issuance back toward normalization.

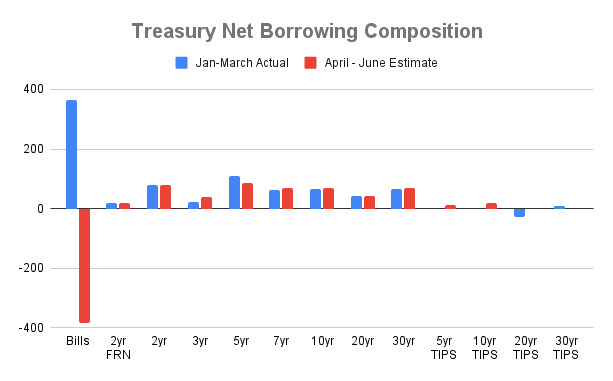

As seen in the chart below of the estimate for borrowing for the next two quarters, Bessent has toed the line and kept the policy approach he criticized Yellen for:

What’s even more interesting is the commitment to the forward guidance of this issuance that was introduced last year, guidance the Treasury decided to keep despite recommendations from TBAC to remove it:

“In discussing issuance recommendations, the committee uniformly encouraged Treasury to consider removing or modifying the forward guidance on nominal coupon and FRN auction sizes that has been in the refunding statement for the past four quarters. Some members preferred dropping the language altogether to reflect the uncertain outlook, though the majority preferred moderating the language at this meeting.”

Despite this recommendation, Treasury kept the following commitment:

“Based on current projected borrowing needs, Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.”

So what’s the takeaway? I’ll leave it with a meme:

— Felix Jauvin

As the US financial system adapts to the rise of digital assets, institutional leaders are making their next big moves. What role will crypto play in global markets? How are fund managers positioning for the future?

At DAS NYC, you’ll hear directly from decision-makers at VanEck, Brevan Howard, and Binance as they unpack the evolving regulatory, macro, and investment landscape. From ETFs to onchain finance, these conversations will define the next era of institutional crypto.

Don’t just watch from the sidelines, be in the room where it happens.

📅 March 18-20 | NYC

This is Ark Invest’s “base case” 2030 price target for bitcoin, according to its “Big Ideas” report published this week.

Ark’s bear and bull cases for BTC price five years from now are $300,000 and $1.5 million, respectively.

These three targets assume various institutional investment levels (1%, 2.5%, 6%), as well as different possible allocations to BTC from nation-state and corporate treasuries.

First, MicroStrategy rebranded to, well, just Strategy. Then it detailed its plans for 2025.

If you weren’t yet convinced the company formerly known as MicroStrategy was all in on bitcoin, perhaps yesterday changed that.

Strategy’s orange logo features a bitcoin “B.” Company leaders, after Wednesday’s market close, pledged to stick with its plan to raise, purchase, and repeat.

The self-proclaimed bitcoin treasury company (and now a Nasdaq 100 stock) held 471,107 BTC, as of Feb. 2 — worth roughly $46 billion at that time. It acquired 258,320 for $22.1 billion in 2024 (avg. price of $85,447 per BTC).

On yesterday’s earnings call, Strategy CEO Phong Le reiterated the company’s 21-21 plan detailed in Q3 — raising $21 billion of equity and $21 billion from fixed income securities between 2025 and 2027. Strategy has made progress there faster than anticipated due to “favorable market dynamics,” he noted.

The capital-raising/BTC-buying ramp-up in Q4 was clear. Strategy raised $15 billion through equity issuances and $3 billion via convertible debt. It had raised $10 billion over the previous 17 quarters (dating back to first adopting BTC as its treasury reserve asset).

The company is shifting its focus in 2025 to fixed income issuances (i.e. convertible notes, preferred stock), Le said. Its long-term leverage target is 20-30% of its BTC holding value.

In a Thursday research note, Benchmark’s Mark Palmer pointed to Strategy upping its 2025 BTC yield target to at least 15% — up from the 6-10% figure it offered on the last earnings call.

Though Strategy paused its BTC-buying spree last week, Palmer said the company’s $10 billion BTC dollar gain target (quantifying shareholder value created by its treasury operations) implies it will continue to “aggressively” raise capital to fuel BTC buys.

Palmer kept his price target for MSTR (the ticker remains) at $650. The stock was trading around $326 at 1:30 pm ET.

Oh, and Strategy wants you to know it’s launched a merchandise store for all your apparel needs. To each their own.

— Ben Strack

Digital assets are not quite like any others. That’s part of what makes them appealing to many — but it can also spur confusion.

Trying to quantify the relationship between BTC, for example, and other asset classes is becoming more prevalent as more investors seek diversification and hedging opportunities.

A clear finding in a recent FTSE Russell report: The rolling correlations of bitcoin and ether returns sharply increased with risk-on assets since 2020.

If we look at BTC in particular, the Russell 1000 index — comprising US large-cap stocks — has a 0.58 correlation to the asset. That relationship is nearly as strong for BTC and US financial stocks and US tech stocks — at 0.53 and 0.52, respectively.

The correlation, since Covid, between BTC and US high-yield credit (the most “risk-on” fixed income asset class) stands at 0.49.

Prior to the Covid-19 outbreak (spurring inflation and monetary tightening), all these correlations were much closer to zero.

7–10 year US Treasurys were rather unique in not seeing a meaningfully higher correlation to BTC after Covid. And the US dollar is the only asset showing negative correlation to BTC and ETH over those years.

Despite bitcoin often being compared to gold, the BTC-gold correlation in the post-Covid era is only 0.15.

BTC’s high volatility (and the varying importance of safe haven and store-of-value characteristics in financial markets) may obscure the “true correlation” between these assets’ returns, the report notes.

It adds: “But the true correlation may simply be low, reflecting the fact that bitcoin and ETH are predominantly risk-on assets, whereas gold has a long-established trading history as a ‘safe haven’ asset, even if they do share some store of value characteristics.”

— Ben Strack

The Bank of England cut interest rates from 4.75% to 4.5% — their lowest point since June 2023. Hargreaves Lansdown’s Susannah Streeter said markets are now pricing in the likelihood of a 3.75% base rate by December, indicating three further reductions.

Trump Media and Technology Group said Thursday it has applied to register trademarks for names related to six investment products, including a “Bitcoin Plus” ETF and SMA.

Ben attended the Ondo Summit at NYC’s Lincoln Center today. Check tomorrow’s Forward Guidance for some of his event takeaways.